|

|

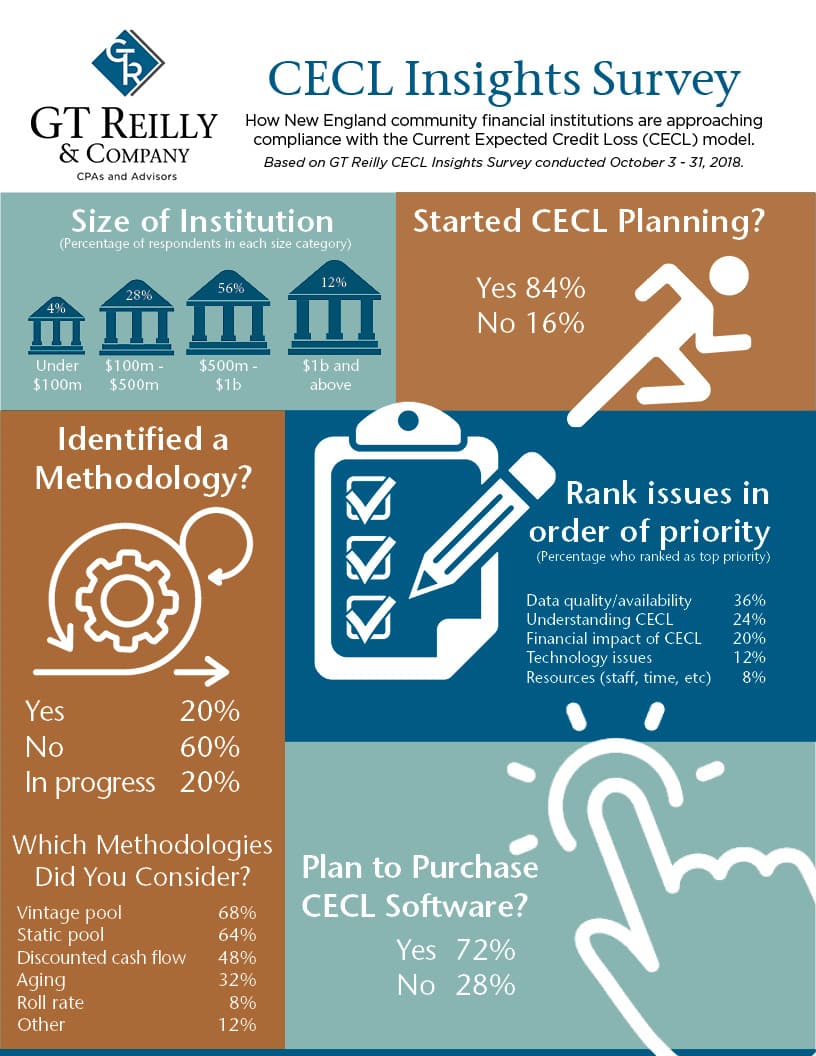

The majority of community banks and credit unions in Southern New England have started planning their adoption of the new Current Expected Credit Loss accounting method, but most have yet to identify exactly how they will implement this new standard.

That was the main finding from a CECL Insights Survey conducted by Milton-based G.T. Reilly & Co., which provides audit and consulting services to community-based financial institutions.

Eighty-four percent of institutions have started planning for CECL adoption, but only 20 percent have identified a specific methodology they will use for meeting the standard, according to the survey.

“CECL represents the most significant change in financial reporting requirements for community banks and credit unions in many years,” Thomas J. O’Connor, CPA and vice president and director of financial institution services for G.T. Reilly, said in a statement. “There is no ‘one size fits all’ approach for adopting CECL. Small institutions will have different needs and resources for meeting the new standard than large institutions will.”

The CECL model, adopted by the Financial Accounting Standards Board in 2016, is a new accounting standard that will change how financial institutions account for expected credit losses. It will require banks and credit unions to take into account forward-looking factors that will help anticipate losses, rather than just historical data on losses already incurred.

The implementation deadline for non-publicly held banks and for credit unions recently was extended to 2022 by the Financial Accounting Standards Board.

In other survey findings, 60 percent of respondents said they have not identified a methodology that fits their institutions’ needs, while 72 percent of respondents say they plan to purchase specialized software to help them comply with CECL.

“The good news is that the vast majority of financial institutions have begun their CECL planning,” O’Connor said. “But clearly they are early in the process and have a lot of decisions to make.”

Only 24 percent of respondents said they were concerned about understanding the CECL requirements and only 20 percent said they were concerned about the costs of CECL compliance. Thirty-six percent of respondents said they believe that data quality and availability – key to complying with CECL – is a significant issue.

Nearly 60 percent of respondents represented institutions with total assets between $500 million and $1 billion, and 12 percent were from institutions over $1 billion. The remainder were from institutions with up to $500 million in assets. Most respondents were top-level financial managers of their institutions, including chief financial officers, vice presidents of finance and controllers.